Many millennials are now approaching middle age as the oldest of them turn 40 this year; thus, retirement discussions should not be delayed any longer.

A retirement plan is non-negotiable regardless of age. Having a smart retirement plan can allow you to take full advantage of retirement at the right time. It is beneficial to plan for retirement now, no matter how old you are, but investing early will allow you to leave your job at the right time, rather than trying to survive through retirement. The earlier you start planning for your retirement, the better.

11 Steps to Planning the Best Retirement.

Start Early

Thinking about retirement early enough is a great way to set yourself up for success by the time you retire. The earlier you start saving, the more likely it is that your savings and investment will compound towards retirement.

By investing in your retirement fund early and allowing the money to grow, you will earn more than someone who opens a retirement account later.

Decide the type of retirement you want

Having a comfortable retirement is expensive. To maintain your standard of living when you stop working, you will need 70 to 90 percent of your pre-retirement income. You can take control of your financial future. Making a retirement plan is crucial to ensuring a comfortable retirement. Deciding on the type of retirement you want will also influence the plans you choose and the types of investments you make.

Utilize your employer's retirement plan

The most common retirement employee retirement plan is the 401k plan which is contributory between employer and employee. If you combine compound interest and tax deferrals, you will accumulate more money over time. Also, find out about your employers’ pension benefits and how they can be applied to your retirement plans.

Consider setting up an Individual Retirement Account

An Individual Retirement Account is a savings account offered by financial institutions, with tax advantages for individuals to save and invest for the long term. In addition to your employer’s contributory retirement plan, it is wise to equally set a portion of your income towards a personal retirement account with a tax advantage.

If you save $6,000 per year at 7% interest in a personal retirement account, you would have $829,421 at the end of 35 years for example.

Individual retirement accounts are particularly useful for small business owners, freelancers, or self-employed individuals who do not have a contributory retirement plan from employers.

Avoid withdrawing from your retirement fund

Try not to withdraw from your retirement fund except in the case of an emergency where there are no other options available. Retirement savings withdrawn now may lose principal and interest, and you may lose tax benefits or incur withdrawal penalties. In case of a job change, leave your retirement money in your current plan, or move it to an Individual Retirement Account or your new employer's plan.

Support your retirement savings with investments

Inflation can have a profound impact on retirement planning because it lowers the worth of your savings. When drawing up your retirement plan, you need to take that into account. Investing is a good way to mitigate the impact of inflation on your retirement savings.

Even though it may seem like a good idea to ignore stocks to reduce risk, stock growth can still be very valuable. As part of your portfolio, you should consider a stable mix of stocks, bonds, mutual funds, and other assets that fit your risk tolerance, and liquidity requirements.

Understand your Retirement Social Security benefits

Retirement social security benefit provides supplemental income, medical care to retirees. Knowing how your government provides social security benefits, or if none are provided, is essential as you plan your retirement.

The amount of social security income you receive depends on;

- How much you earn in your lifetime

- The age at which you begin receiving benefits

- Your eligibility to receive your spouse's benefits instead of your own

Engage the services of a professional

As retirement planning involves your future, it is important to avoid gambling for the sake of minimizing the risk of losses. If you are not capable of personal retirement planning, speak with an investment advisor, a lawyer, an estate planning attorney.

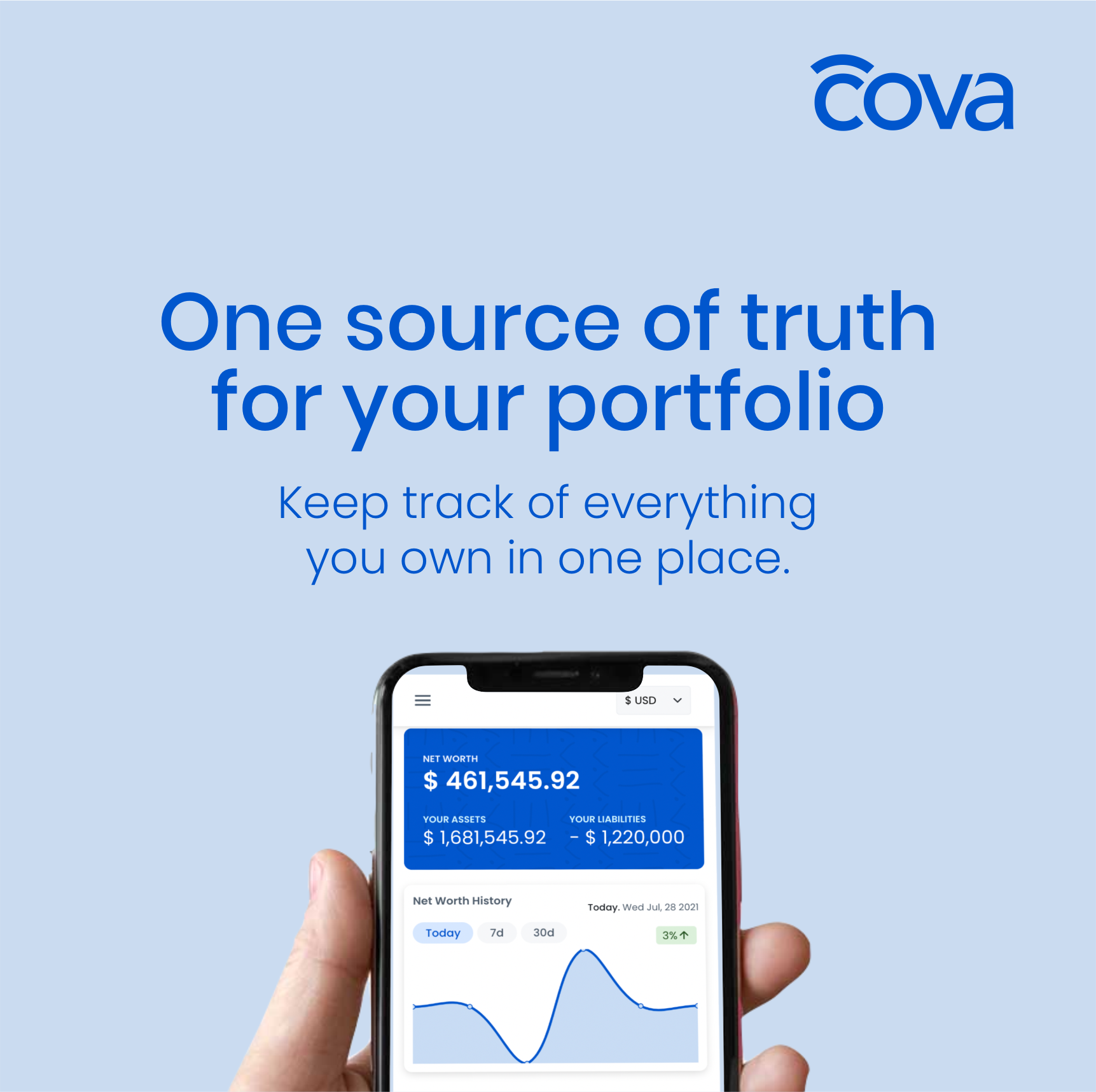

Track everything you own

One key to successful retirement planning is tracking everything you own during your lifetime. Track all your assets, digital and traditional; cryptos, NFTs, stocks, mutual funds, investments, real estate, and liabilities like credit card debts, loans, etc. Organizing everything you own and tracking your net worth help you to understand the true value of your wealth towards retirement. Tracking your assets also gives you information about rebalancing your portfolio for more rewards on investment and paying off your debt.

Cova is a tool that helps you to track everything you own including your liabilities in one place. Seeing the true picture of your wealth in Cova can contribute immensely to successful retirement planning. Cova also helps you track and manage your retirement savings and investments, such that you can keep track of your retirement savings and investment goals in one place.

Plan your Estate and Assign Beneficiaries

Planning your retirement should include a plan on how you wish to transfer your wealth in the case of any eventuality. Not having an estate plan against the wealth you are building for your retirement may result in futility if your loved ones have no information about how to claim your wealth. While traditional estate planning is still effective, millennials now resort to digital estate planning tools like Cova, which allows you to track everything you own in one place, save your passwords and important documents in a digital vault and assign a beneficiary who receives your wealth in the case of any eventuality. Cova is the all-in-one borderless estate planning software for Millennials.

Get your debt under control

Manage your debt, especially your credit card debt, by paying it off

Be sure to keep up with the payments on your loans if you have any. To avoid spending retirement savings on debt financing, plan to pay off any accrued debt before retiring.

Conclusion

Planning for retirement requires a strategy and a high level of attention to detail. In order to retire on time and have enough income to live comfortably after retirement, it is essential to incorporate a retirement plan into your overall financial portfolio now.

{kind=link}